• ONE down payment assistance program that you may use nearly nationwide (not available in WA)

• Completely forgivable grant, equals 2% or 3.5% of purchase price

• May be combined with up to 6% seller concession for closing costs

• No resale restrictions

• ONE down payment assistance program that you may use nearly nationwide (not available in WA)

• Completely forgivable grant, equals 2% or 3.5% of purchase price

• May be combined with up to 6% seller concession for closing costs

• No resale restrictions

The Empowered DPA

Program can be used in

conjunction with:

• FHA 203(b)

• FHA 203(k) Limited

• FHA 203(k) Standard

• FHA Repair Escrow

Program cannot be used in conjunction with: • Non-FHA Loan Types • Any other DPA Program • High Balance Loans • TBD

ELIGIBLE PROGRAMS

The Empowered DPA

Program can be used in

conjunction with:

• FHA 203(b)

• FHA 203(k) Limited

• FHA 203(k) Standard

• FHA Repair Escrow

INELIGIBLE PROGRAMS

Program cannot be used in conjunction with: • Non-FHA Loan Types • Any other DPA Program • High Balance Loans • TBD

BORROWER ELIGIBILITY

To be eligible for the program, the Borrower(s) must meet

only ONE of the four following categories outlined:

First-Time Home Buyer

Current / Retired Employment or Volunteer / Non-Paid Member

Income

Underserved Census Tract

First-Time Home Buyer

Any Borrower on the loan application is a First -Time Home Buyer

who meets the following criteria:

Is purchasing the Subject Property

Will reside in the Subject Property as their principal residence

Has had no ownership interest (sole or joint) in a residential

property during the three -year period preceding the date of the

application

Or is an individual who is a homemaker or single parent that has no

ownership interest in a principal residence (other than a joint ownership

interest with a (former) spouse) during the three -year period preceding

the date of the application.

Current / Retired Employment or Volunteer / Non-Paid Member

Any Borrower on the loan application is a

current, retired, volunteer or non -paid:

Military personnel

First responder (police officer, firefighter, public safety officer,

paramedic, emergency medical technician (EMT) or similar

Educator (Sunday school teacher, tutor, day care provider)

Medical personnel (nurse, doctor, X-Ray technician, hospital

administrator, or similar)

Civil servant in a Federal, state or local municipality

Income

The Borrower’s income (or, in the event of multiple

Borrowers on a loan application, their income

collectively) is equal to or less than 140% of the state or

county median income regardless of family size based

upon the state or county where the Security Property is

located.

The Borrower’s income (or, in the event of multiple

Borrowers on a loan application, their income

collectively) is equal to or less than 140% of the state or

county median income regardless of family size based

upon the state or county where the Security Property is

located.

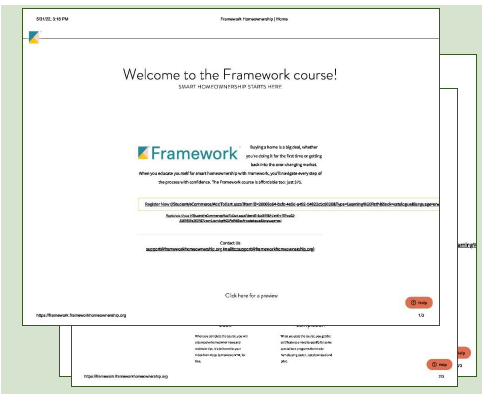

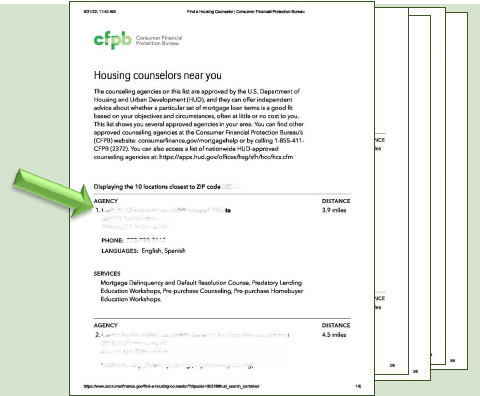

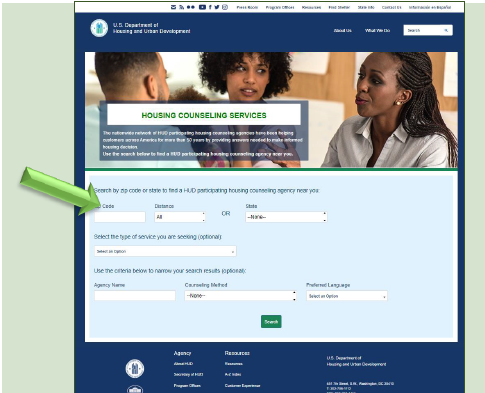

FRAMEWORK HOMEOWNERSHIP and HOMEOWNERSHIP COUNSELING LIST offer HUD approved Homebuyer Counseling disclosure courses. This disclosure lists the 10 closest Housing Counselors near the subject property zip code OR you can visit HUD.GOV . For this program, you will need to ensure the course completed is either the “Pre -purchase Homebuyer Education Workshop” or the “Pre -purchase Counseling”.

FRAMEWORK HOMEOWNERSHIP and HOMEOWNERSHIP COUNSELING LIST offer HUD approved Homebuyer Counseling disclosure courses. This disclosure lists the 10 closest Housing Counselors near the subject property zip code OR you can visit HUD.GOV . For this program, you will need to ensure the course completed is either the “Pre -purchase Homebuyer Education Workshop” or the “Pre -purchase Counseling”.

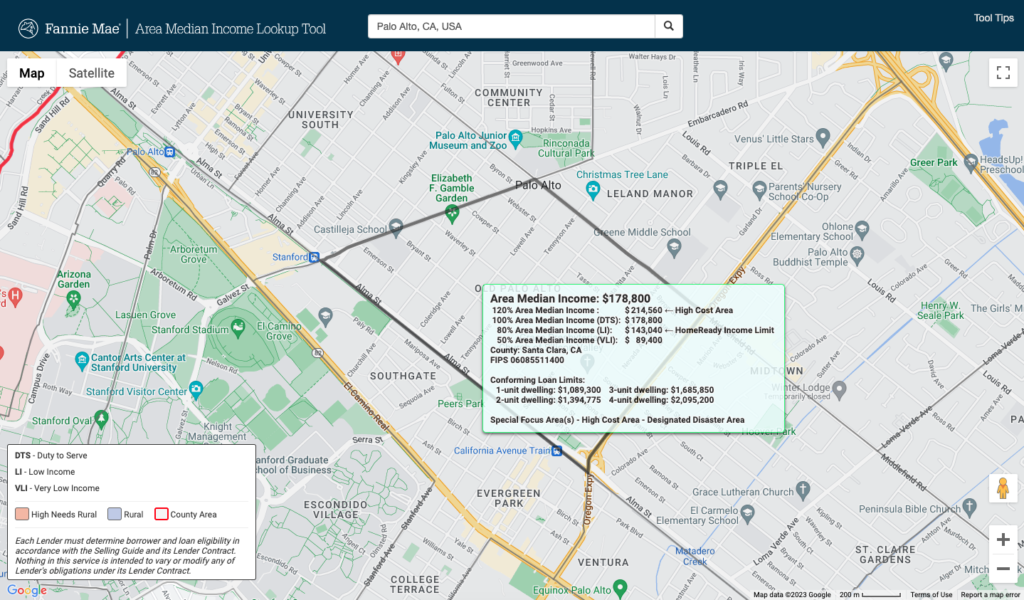

Income Limit will populate. • Borrower’s income (or, in the event of multiple Borrowers on a loan application, their income collectively) must be equal to or less than 140% of the state or county median income regardless of family size based upon the state or county where the Security Property is located to be eligible based on income.

Example below:

$178,800.00

X 140%

$250,320.00

FREQUENTLY ASKED QUESTIONS

Q: If I previously completed a Homebuyer Counseling course, will it be accepted?

A: If you have completed the course prior to our application date, it will be accepted if it is a HUD approved course, and the expiration of the course is prior to the Note Date.

Q: Do all Borrowers need to take the home counseling or just one?

A: Only one Borrower is required to complete the course.

Q: Can I contribute more than 3.5% for their down payment?

A: Yes, you are permitted to contribute more than the minimum required investment of 3.5%.

Q: Are additional disclosures required?

A: Yes, there are 3 additional disclosures required for the Empowered DPA program. The first disclosure will be provided when the loan is setup and the other two disclosures will be provided after underwriter approval and must be printed out and wet signed.

Q: Does the program allow for a non-occupant co-Borrower?

A: Yes, the program will allow for a non-occupant co-Borrower.

Q: Do all borrowers on the loan need to meet 1 of the 4 eligibility requirements? (First time homebuyer, Income, Underserved or Employment?)

A: Only one Borrower is required to meet 1 of the 4 areas to be eligible.

Q: Is TBD permitted?

A: TBD is not permitted because it must be an Approve/Eligible, which requires complete property information.

Q: Are we going to take the AMI and multiply it by 140% to determine our income limit for this program regardless of the areas being underserved? Are underserved areas exempt from the income limits?

A: No, use 140% of the AMI in all areas.

Q: Do we need confirmation of wire Instructions prior to DPA funds disbursement?

A: Yes, the lender will confirm the settlement agents / Title companies wire instructions prior to the DPA funds being requested

This website uses cookies to enhance user experience and to analyze performance and traffic on our website. We also share information about your use of our site with our social media, advertising and analytics partners. By clicking "Accept Cookies", you consent to the use of ALL the cookies.Accept CookiesDecline All Non-Essential Cookies